December 2014

Welcome to the CFALA e-newsletter, a periodic publication with stories about noteworthy events and programs sponsored or hosted by the society, guest articles by members, book reviews, and other items of interest to CFALA members. Click on the headlines below to read the full stories. And if you’d like to contribute a story suggestion or, even better, write an article, we’d love to hear from you. Please email Executive Director Laura Carney at laura@cfala.org.

*Please note that the content of this e-newsletter should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Society Los Angeles.

In this issue ...

Can I Trust My Financial Advisor?

Recent surveys from CFA Institute and Edelman (See The Edelman Trust Barometer - 2014) suggest that the financial services firms and banks are the least trusted industries. In view of this reality, taking a deeper dive into the ordinary process of due diligence – and identifying a more thoughtful way for investors to pursue the process in their due diligence process for advisory services is a good idea. We in the advisory business should welcome the opportunity to help shape that process.

There is an informative new resource available from Charlotte Beyer in her newly released book, Wealth Management Unwrapped (hyperlink is to the Amazon listing). Additionally, she provides a perspective piece for advisors (appendix) which coordinate advisory responses in assessing emotional capacity and sophistication of the client – both of which are extremely crucial in formulating the process by which their investment management process is framed.

Note also that Charlotte and others from the CFA Institute have outlined their suggestions for designing and implementing investment policy statements for advisors. You can review the information available at the following link – Investment Policy Statements.

One personal observation, I think there are essentially two general descriptions of professionals at opposite ends of the scale in the investment business. Simply put, there are –

-

“TRADERS” (Portfolio Managers/brokers/traders) – usually compensated as percentage of assets, growth in value, or per trade. Primary Focus is on markets, values, and investments. Job is to pick winners and make money via a specific strategy. It would seem to me that “suitability” may be the appropriate standard from a legal/compliance standpoint.

AND/OR

-

“INVESTMENT ADVISORS” – can be fee only, percentage of assets, or possibly on the basis of trades. Primary Focus is on clients and their needs. The professional role starts with basic discovery (psychological and financial profiling) for each client combined with the subsequent formulation of the client’s perspective into a portfolio structure appropriate to meet their long-term horizon needs – anticipating uncertainty in predicting accurately economic/market fluctuations. Investment advisors do need an active inventory of resources for “TRADERS who are deemed appropriate to selectively engage for clients. “Fiduciary” is the standard appropriately applied to this form of professional role.

Frankly, the industry does a lousy job differentiating between these two functions. The term “advisor” has been applied to both. A closer look at what is needed is an important element required in order to clarify how much and which function you wish to engage. From my experience, most individuals have not gone down the path sufficiently to know what they want or need.

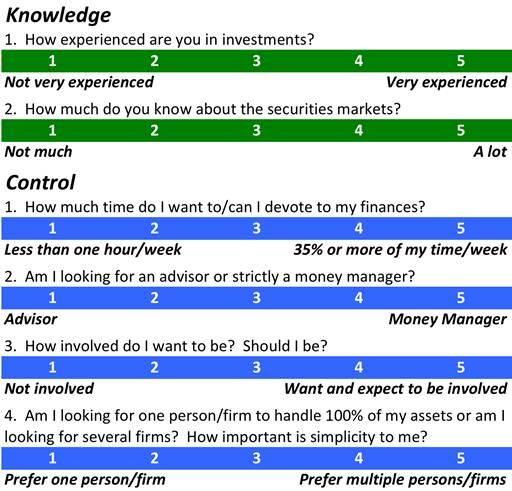

One important starting step is to formulate the client’s assessment of their knowledge/sophistication and the need for control. Specifically, a self-assessment based on the following questions –

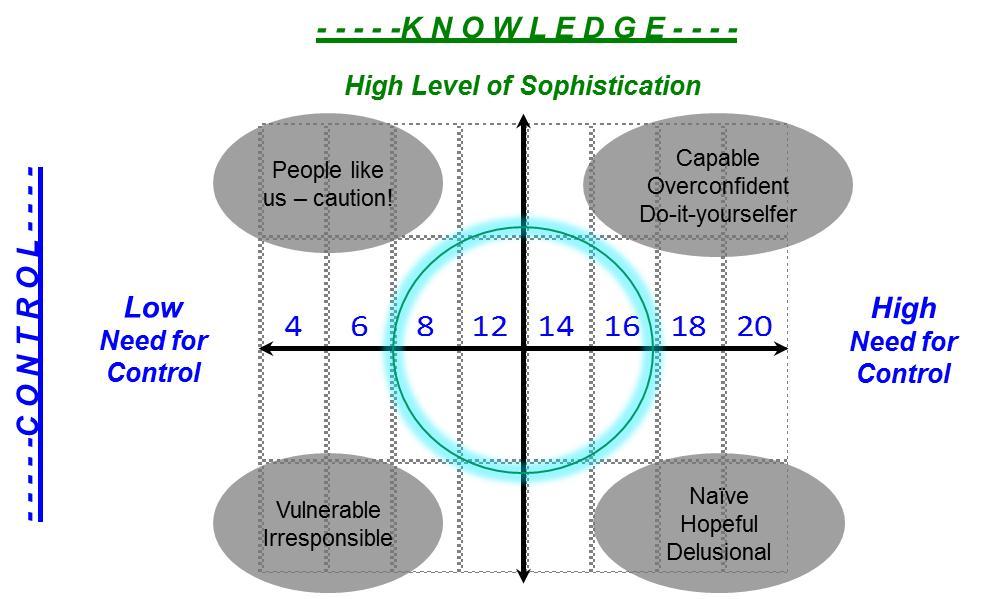

Add the scores for each category and plot the result on the following graph:

The optimum is to fall within the middle circle. To the extent that an individual’s assessment falls toward the external quadrants, the risks of that position are identified – and obviously from either a self-management, or advisor perspective they will need some periodic and additional evaluation. Undoubtedly, the advisor will need some more expertise in behavioral management.

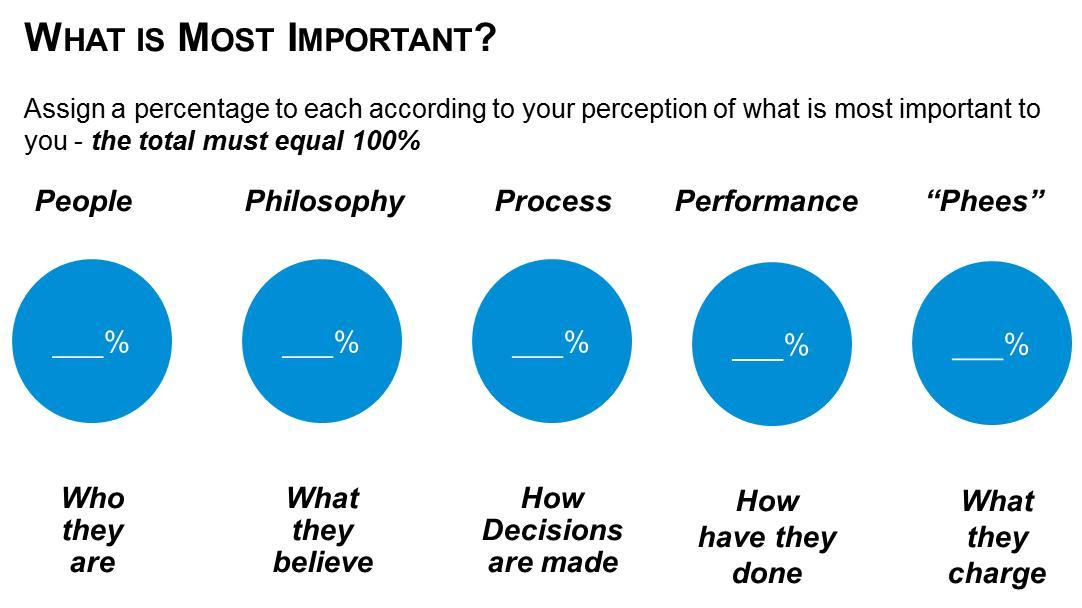

An additional graphic illustrates a handy way for a potential client to prioritize what is important to them in hiring an advisor. Advisors can then respond much more efficiently in providing select information that is most relevant to their potential client:

Finally, there are a select number of questions appropriate for potential clients to ask their advisors. By being prepared to address these, advisors may also be more effectively prepared to align themselves with clients who are a better fit.

Suggested Advisor Questions (Note: Some questions from Charlotte Beyer, some from the author of this newsletter piece)

-

What are your qualifications and certifications? Can you name one or two real life experiences that were most helpful to enhancing your professional skills?

-

What regulatory body oversees you? SEC? OCC? Other?

-

Do you operate under the fiduciary standard in client relationships?

-

What are the top three activities in your service routine that you believe add the most value to your clients?

-

Do you utilize written investment policy statements with your clients? How do you determine the target return (after inflation) for my overall portfolio?

-

How do you define risk? How would you manage it in my situation?

-

How do you access the best funds or smartest money managers? What criteria do you use (and frequency) in deciding/monitoring which ones to use?

-

What are your long-term career objectives and do you have a succession plan?

-

Are your investment strategies based on a global perspective? How do you view active vs passive investment strategies?

-

How do you ensure your technology is state of the art?

-

What are your fees? Are there additional indirect fees we pay for specific investments? How frequently do you review fees with your clients?

If you have an interest in taking a deeper dive into these topics, pop an email to the advocacy/ethics committee chairman, Dan Pomerantz at pomerantz@bessemer.com.

Why Most Active Money Managers Underperform

Experience (and the Level 3 curriculum) tells us that most individual investors are not as rational as what traditional finance theory suggests. In traditional finance theory, investors are assumed to have access to perfect information and process that information without bias or emotion. On the other hand, behavioral finance challenges the idea that investors are rational.

What about professional money managers? Surely they are more rational and not susceptible to emotional biases or cognitive errors. According to a 2013 article entitled “Understanding How the Mind Can Help or Hinder Investment Success” by Vanguard Asset Management, even professional money managers are susceptible to many of the same biases and cognitive errors that affect the average investor.

Considering the author, it is interesting that the Vanguard article did not aim to prove that passive management is somehow better than active management.. Rather, the article attempted to illustrate that active money managers underperform their respective benchmarks at least partly due to behavioral biases. According to a 2012 Forbes article entitled “Indexes Beat Active Funds Again in S&P Study,” 81% of active mid-cap funds underperformed the S&P Midcap 400 Index over a 5-year period. There are numerous behavioral biases or factors (anchoring, illusion of control, disposition effect, confirmation bias, etc.) to which most investors are susceptible, but two biases seem to apply particularly to professional investors: herd behavior and overconfidence.

HERD BEHAVIOR

Herd behavior describes the tendency for individuals or groups to mimic the actions of a larger group. Most money managers do not blindly mimic the actions of other successful money managers, but in some cases, clients may ask for a similar, successful strategy. In general, “winners” are observed very closely and as more investors are attracted to them, no one wants to fight against the power of an increasing majority.

Herd behavior can also be observed within a money management firm. I have experienced this behavior first hand as a member of the investment committee at a firm some years ago. Some investment decisions were made by consensus – for example, the committee members were to vote to include investment XYZ in our portfolio. Normally the CIO would make his case first and vote yes, and the next person would follow the same process and make his vote, and so on. More times than not, a vast majority would vote the same direction as how the CIO voted. Even though independent thinking and analysis were encouraged, when it came time to vote, most would not go against the crowd, led by the CIO.

John Maynard Keynes once said “Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally.” When the majority ends up doing the same thing (knowingly or unknowingly), they’re likely to achieve mediocre results.

OVERCONFIDENCE

Regarding overconfidence, Robert Shiller simply said, “People think they know more than they do.” Overconfidence is a trait that can be observed in many facets of life. For example, according to a 2007 Foreign Policy article entitled, “Why Hawks Win” by Daniel Kahneman and Jonathan Renshon, more than 80% of the participants in a survey believe themselves to be above average with respect to their driving skills. Just as most people consider themselves to be above average with respect to their driving skills, similar statistics can be found with regards to one’s gambling skills, test-taking skills, etc.

Not surprisingly, overconfidence is also very pervasive in the investment industry. In a 2006 study entitled “Behaving Badly,” James Montier found that 74% of the 300 professional money managers surveyed believed that they had delivered above-average performance. Overconfident investors tend to believe they can influence outcomes over which they clearly have no control. Unfortunately, overconfidence can lead to reduced returns and increased risks. There are a number of ways that this can occur.

Based on a few recent “winners,” confidence can easily turn into overconfidence. One may start acting as if they have a magic touch, often confusing luck with skill. While these money managers’ investment decisions may be based on sound analysis or research, overconfidence can lead to underestimating risks of certain volatile assets and therefore inappropriately overweighting those assets in a portfolio.

Overconfidence also influences trading decisions. Overconfident managers have the illusion of adding value (alpha) by frequent trading. One cannot overlook transaction costs associated with an increased trading activity. In order to compensate the transaction costs, these tactical trades need to generate higher returns. A number of studies have shown that for a vast majority of these managers, frequent trading does not add value after adjusting for the friction.

CONCLUSIONS

Martin Sewells defined behavioral finance as the study of the influence of psychology on the behavior of financial practitioners and the subsequent effect on markets. Many of the key concepts behind behavioral finance have been around for years, going back to the early work of Daniel Kahneman and Amos Tversky. Richard Thaler and others have also contributed to the development of the field over the years.

One of the criticisms of behavioral finance has been that although behavioral finance does a fair job of explaining what went wrong after the fact, it’s difficult to apply its core ideas in a practical, consistent manner. However there are a lot of new and exciting research efforts taking place today in the area of practical applications of behavioral finance (the details are beyond the scope of this article), and over the coming years practitioners should take heed.

To be sure, there are skilled managers out there who consistently beat their benchmarks. However, studies have shown that most active money managers underperform. Behavioral finance appears to be playing a role in that underperformance, and understanding how behavioral finance plays a role in portfolio management may help remedy the inability to beat the market.

By Stan Yang, CFA, CAIA, - Director of Trading for Savos Investments, a division of AssetMark, Inc. The views expressed in this article are Stan’s and do not represent Savos or AssetMark.

Fiduciary Standard for Investment Professionals

Recently I was asked to review a portfolio recommendation for an acquaintance, Julie. The recommendation was made by her registered representative, Bob.

Julie has a 403b (variable annuity) with a local school district worth approximately $100,000. Bob suggested that she roll it into an IRA and fund a single Class 'A' share utility mutual fund. This is what I discovered:

· Bob just took over this book of business from another financial advisor.

· Had Julie done this roll over, it would have put $4,000 immediately into Bob's pocket.

· Bob thought Julie was in a fixed annuity. Bob is her registered representative, but he didn't know she was in a variable annuity with sub accounts available. She could have just as easily chosen a utility fund from among her currently available sub accounts.

· Julie is under age 59 1/2 so doing a roll over is impossible, unless she leaves her current job. Bob didn't know that either.

Bob sounds like an ignorant salesperson, doesn't he? But he has a bachelors in economics from UC Berkeley, has done graduate study at Wharton, and he is a Certified Financial Planner (CFP).

Why would Bob suggest such a thing? It might have something to do with the IRS lien for more than $40,000 for not filing his quarterly estimates.

My fear is that Bob is making similar recommendations to other clients of his newly acquired book of business.

How is this possible? Shouldn't Bob have recommended the less expensive option for Julie? The key point here is that Bob is a registered representative with a brokerage firm, not a Registered Investment Advisor (RIA). He is held to the much lower “suitability’ standard,” versus the “fiduciary standard” of an RIA. The class 'A' fund is suitable for Julie, even though it would cost her an additional $4,000.

This really needs to change. CFA Institute has been lobbying for a universal fiduciary standard for financial professionals who provide investment advice, particular to retail clients (See http://tinyurl.com/ky9apru). This should apply regardless of the individual’s registration. It’s time for the financial services industry to take this step toward putting clients first.

By Don Steinmann

The CFA Institute has recently expanded its free, interactive, case-based ethical decision-making webinars to include a Part II, which explores additional case studies. The new webinar is based on Robert Prentice's (Financial Analysts Journal 2007) article, "Ethical Decision Making: More Needed than Good Intentions." Read more... And more...

What Doctors and Families Have That Advisors Don't

ThinkAdvisor's Gil Weinreich reports on the CFA Institute's efforts to foster relationships of trust between investment advisors and their clients. In his article, Weinrich relays comments from Robert Stammers, CFA, Director of Investor Education for the CFA Institute. Weinrich also provides links to the 2014 Edelman Trust Barometer results for the financial services industry, as well as the CFA Institute's Statement of Investor Rights campaign. Read more... And more...

Finance and the Jelly Bean Problem

In his column, The Undercover Economist, Tim Harford provides a highly readable account of Cambell Harvey, Yan Liu, and Heqing Zhu's (2014) examination of 296(!) factors previously found to have a significant role in explaining the cross-section of expected equity returns. (The referenced study can be downloaded from SSRN by doing a QuickSearch on abstract ID 2249314). Read more... And more...

In its Resilience by Design report, Los Angeles Mayor Eric Garcetti's Seismic Safety Task Force discusses the city's earthquake-related vulnerabilities in four areas: buildings, water, and communications. Their review of the potential impacts of the so-called "ShakeOut scenario" -- a magnitude 7.8 earthquake on the southern San Andreas Fault -- makes for riveting reading. Read more... And more...

Why Frozen Is so Appealing

A year after its November 2013 release, the Disney animated movie, Frozen, continues to attain new pop culture milestones (e.g., Time Magazine's Most Influential Fictional Character of 2014). In his blog, Wayward Fancies, Raymond "The Minstrel Boy" Dokupil takes a closer look at the elements that give the film so much more appeal than it might otherwise warrant. Read more... And more...